The income summary is the summarized version of revenues earned by the business and the expenses incurred by the business. It is a temporary summary account, and the netted values are always transferred to the capital account of the income statement. If you are using accounting software, the transfer of account balances to the Income Summary Account is handled automatically whenever you elect to close the accounting period. It is entirely possible that there will not even be a visible income summary account in the computer records. It is also possible that no income summary account will appear in the chart of accounts.

Answer the following questions on closing entries and rate your confidence to check your answer. Josh Pupkin is a member of WSO Editorial Board which helps ensure the accuracy of content across top articles on Wall Street Oasis. Josh has extensive experience private equity, business development, and investment banking This content was originally created by member WallStreetOasis.com and has evolved with the help of our mentors. My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers.

AccountingTools

Income summary account serves the purpose of ensuring the correct calculation of profit and loss. Transferring account balances directly to the retained earnings account increases the chances of missing some of the accounts, which can paint a completely different picture on profit and loss for a given period. Income summary is a holding account used to aggregate all income accounts except for dividend expenses.

We will debit the revenue accounts and credit the Income Summary account. The credit to income summary should equal the total revenue from the income statement. After Paul’s Guitar Shop prepares its closing entries, the income summary account has a balance equal to its net income for the year. This balance is then transferred to the retained earnings account in a journal entry like this. Likewise, shifting expenses out of the income statement requires one to credit all of the expense accounts for the total amount of expenses recorded in the period, and debit the income summary account.

Why is it important to close certain accounts at the end of the year?

Let’s extend the

example of Company X, which had a $44,000 profit in its first year of

operations. Let’s now assume that, in its second year of operations, the

company incurs $2,000 of interest expense and $15,000 of cost of goods sold

expense while gaining $55,000 in sales revenue and $6,000 in investment income. The balance in Retained Earnings agrees to the Statement of Retained Earnings and all of the temporary accounts have zero balances. I imagine some of you are starting to wonder if there is an end to the types of journal entries in the accounting cycle! So far we have reviewed day-to-day journal entries and adjusting journal entries. While both the income summary and income statement provide a report on the net profit and loss of a company, they differ a great deal.

When you manage your accounting books by hand, you are responsible for a lot of nitty-gritty details. One of your responsibilities is creating closing entries at the end of each accounting period. This net balance of income summary represents the net income if it is on the credit side.

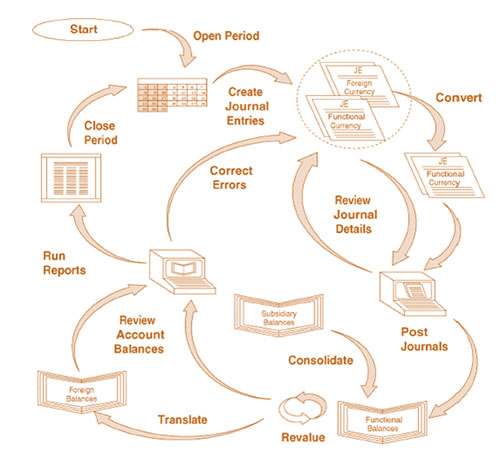

The closing process and Income Summary account

This will be identical to the items appearing on a balance sheet. The credit balance of the revenue account is transferred by debiting the revenue account and crediting the income summary account. Similarly, the debit balances on the expense’s accounts are transferred and zeroed out by debiting the income summary and crediting the individual expenses account. It is a temporary, intermediate account, which means that the revenue and expenses balance is transferred to permanent accounts at the end of the accounting period through closing entries. The closing entries are the journal entry form of the Statement of Retained Earnings. The goal is to make the posted balance of the retained earnings account match what we reported on the statement of retained earnings and start the next period with a zero balance for all temporary accounts.

Temporary accounts are used to record accounting activity during a specific period. All revenue and expense accounts must end with a zero balance because they are reported in defined periods and are not carried over into the future. For example, $100 in revenue this year does not count as $100 of revenue for next year, even if the company retained the funds for use in the next 12 months. Now that Paul’s books are completely closed for the year, he can prepare the post closing trial balance and reopen his books with reversing entries in the next steps of the accounting cycle. After this entry is made, all temporary accounts, including the income summary account, should have a zero balance.

Conversely, if the income summary account has a net debit balance i.e. when the sum of the debit side is greater than the sum of the credit side, it represents a net loss. In partnerships, a compound entry transfers each partner’s share of net income or loss to their own capital account. In corporations, income summary is closed to the retained earnings account. The main difference between the two has to do with the fact that an income statement is a permanent account that highlights all the income and expenses. The income summary, on the other hand, is a temporary account that compiles revenues and expenses. If your revenues are less than your expenses, you must credit your income summary account and debit your retained earnings account.

How do you record income summary account?

The debit to income summary should agree to total expenses on the Income Statement. We see from the adjusted trial balance that our revenue accounts have a credit balance. To make them zero we want to decrease the balance or do the opposite.

Dividend Income Summary: Lanny’s May 2023 Summary – Seeking Alpha

Dividend Income Summary: Lanny’s May 2023 Summary.

Posted: Sat, 03 Jun 2023 07:00:00 GMT [source]

However, each temporary account can be reset thanks to closing entries and begin the next accounting period with a zero balance. When doing closing entries, try to remember why you are doing them and connect them to the financial statements. To update the balance in Retained Earnings, we must transfer net income and dividends/distributions to the account. By closing revenue, expense and dividend/distribution accounts, we get the desired balance in Retained Earnings. This account is a temporary equity account that does not appear on the trial balance or any of the financial statements.

The Entries for Closing a Revenue Account in a Perpetual Inventory System

That way, your next accounting period does not have a balance in your revenue or expense account from the previous period. For the rest of the year, the income summary account maintains a zero balance. This final income summary balance is then transferred to the retained earnings (for corporations) or capital accounts (for partnerships) at the end of the period after the income statement is prepared.

Bert’s May 2023 Dividend Income Summary – Seeking Alpha

Bert’s May 2023 Dividend Income Summary.

Posted: Tue, 06 Jun 2023 07:00:00 GMT [source]

The company can make the income summary journal entry by debiting the income summary account and crediting the retained earnings if the company makes a net income. We need to complete entries to update the balance in Retained Earnings so it reflects the balance on the Statement of Retained Earnings. We know the change in the balance includes net income and dividends. Therefore, we need to transfer the balances in revenue, expenses and dividends (the temporary accounts) into Retained Earnings to update the balance. Each of these accounts must be zeroed out so that on the first day of the year, we can start tracking these balances for the new fiscal year. Remember that the periodicity principle states that financial statements should cover a defined period of time, generally one year.

This way each accounting period starts with a zero balance in all the temporary accounts. In the final netted value column, whether a debit or credit, the amounts would then be transferred to the capital account of the business, and the parallelly, the income summary would be closed out or terminated. As the tables show, this business made a profit during the accounting period. As a result, the business credited its revenue account more than it debited its expenses account, leading to a credit balance. Once a company determines whether it has sustained a loss or earned a profit, the results from the final account are typically transferred into retained earnings on the balance sheet. At the end of each financial year, the temporary accounts in the general ledger must be closed, and the beginning balances of the permanent accounts transferred to the general ledger of the next period.

- It can also be called the revenue and expense summary since it compiles the revenue and expenses that stem from the operating and non-operating business functions.

- Balances from temporary accounts are shifted to the income summary account first to leave an audit trail for accountants to follow.

- Go a level deeper with us and investigate the potential impacts of climate change on investments like your retirement account.

- You need to create closing journal entries by debiting and crediting the right accounts.

- The income summary account holds these balances until final closing entries are made.

- To add something to Retained Earnings, which is an equity account with a normal credit balance, we would credit the account.

The income summary account is a temporary account into which all income statement revenue and expense accounts are transferred at the end of an accounting period. The net amount transferred into the income summary account equals the net profit or net loss that the business incurred during the period. Thus, shifting revenue out of the income statement means debiting the revenue account for the total amount of revenue recorded in the period, and crediting the income summary account. The income summary account is prepared by debiting revenue accounts and crediting expense accounts.